What happens if you make a good income but can’t get ahead? (Or even fall further and further behind each month?)

Andy from Marriage Kids and Money recently discussed a question of the month from Julie that covered exactly that. She and her husband make a good income, but can’t get ahead. And she is clearly frustrated — both with the personal finance world and the current economy.

You can read her full question & Andy’s response here (and listen to the podcast) but I’m going to pull a few things from the question to respond to here. Because I have a lot to add.

Fair warning: there’s some tough love coming in this post. But I’ve also got some specific ideas that could help, plus food for thought in general.

Let’s summarize Julie’s situation a little first.

Julie’s family of three (including one baby) has a $92,000 household income. They live in a “crummy small 2 bedroom rental with poor heat and cracks in the walls” that they pay $1,700 a month rent for. She uses a combination of driving + public transit to get to work, and her husband drives. This eats up a lot of their time. They are spending $470 a month on gas + transit, and $380 a month on car insurance. There’s no mention of a car payment, so I’m going to assume their 2 cars are paid off. I hope that’s not wrong.

She doesn’t say her location, but it’s in a major city with public transit, and monthly parking available for $300. Based on that info, their rent, her transit times, and the mention of heat, my wild guess is that she’s in the Denver or Seattle area. (Assuming it’s a typical rent.)

Their take-home pay is $5,320 per month, and the monthly expenses she listed add up to $5647 a month, including $482 in student loan payments and $1,125 for part time daycare.

Basically, they’re at least $327 in the hole every month.

But it’s worse than that.

She’s left off the costs of several other known expenses. And I suspect she’s also forgotten quite a few other expenses, but who knows. (It’s hard to know everything unless you track your spending, which I highly recommend.)

So although they have a good household income, they’re falling further and further behind. Every single month.

The main thing though? Julie is frustrated.

She’s upset with her situation, the personal finance articles she reads, and the world in general.

“Tell me how to do better”, she says, before giving an incomplete list of the expenses she’s identified.

Then:

Give me an answer other than ‘budget better or make more’ or ‘unroot your whole family and leave your jobs and support system to go somewhere you’ll be unhappy’.

Get it through your head the pull up your bootstraps advice no longer works.

STOP THESE RIDICULOUS USELESS ARTICLES. Say it like it is. Unless you making over $200k or born into it, you’re screwed. Our current economy and the world doesn’t work like it used to.

And I get it.

While I don’t agree that you’re screwed if you aren’t “born into it” or making over $200k, she’s right that our current economy and the world DON’T work like they used to.

College, housing, and health care costs are through the roof, while wages are not. Benefits are often poor, or not even available if you’re in the gig economy. Daycare is expensive (although I personally feel like that’s always been hugely expensive, so maybe not a change there, but not good either way.)

The wealth gap is widening more and more.

The haves have everything they can dream of, and the have nots…don’t. Meanwhile, the middle struggles along, trying to stay on the balance beam.

It IS hard, for so many people.

Many, many, MANY people. Even people who make a good income, especially if they’re saddled with student loans or don’t live in a low cost of living area.

And it’s absurdly hard for people who don’t make much.

When you’re struggling with poverty and/or stratospheric healthcare costs, reading articles that tell you to just skip the daily Starbucks or to eat out less are frustrating.

BECAUSE YOU DON’T EVEN DO THOSE THINGS!

(Budget better with WHAT? It’d be laughable if it weren’t so sad.)

Instead, you’d love to just be able to buy something you like to eat at the grocery store once in a while. Or to be able to have 3 meals a day, of anything. Or to work any job without using all your spoons, let alone get a second one.

Telling someone without any boots to just pull themselves up by their bootstraps IS ridiculous, at best.

And I would never do that.

But Julie doesn’t appear to be in that situation.

So I’m going to address her situation instead here, to the best of my knowledge.

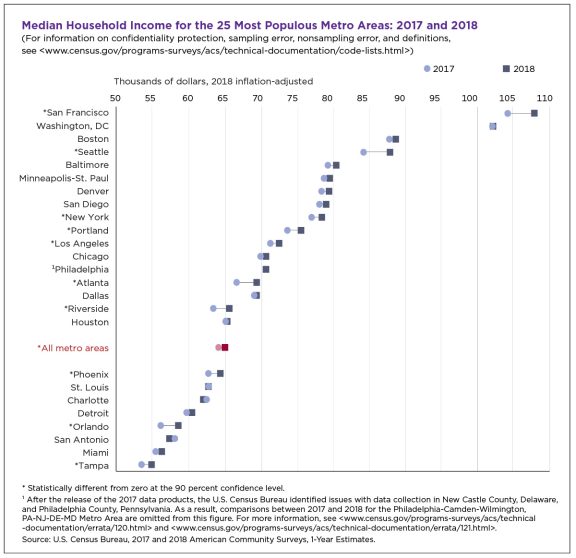

Julie’s family makes more than the median household income of 23 of the 25 most populous metro areas in the United States.

Julie’s family makes more than the median household income of 23 of the 25 most populous metro areas in the United States.

Significantly more, not just a couple thousand more.

And it appears that the only debt her family of 3 has is student loans. (How much, who knows. The total could be staggering for all I know.)

But unless she really lives in DC or San Francisco, she has nice boots. And even if she does live in DC or San Francisco, she at least has cheap boots! In other words, those fabled bootstraps could be a possibility for her.

Especially since she also mentions having a support system, which is huge.

(Many of the bootstrap-style success stories do involve having a helpful support system. People who can feed you, watch your kids, give you a roof over your head if you end up homeless, help you repair your car, lend you a cup of sugar, get you an in with investors, employers, and colleges, you name it.)

So I don’t think her problem is quite what she thinks it is.

However, Julie DOES have a problem, and it’s a big one.

Her problem is that she’s not even living paycheck-to-paycheck.

Instead, she’s in the hole every month. Every single month. Probably more than she realizes.

They have a good income, but can’t get ahead because their expenses are so high compared to that income. Rent and daycare take up 53% of their take home pay. Add in the costs of getting to work, and they’re at 69% of their take home pay.

That doesn’t leave a whole lot for everything else.

Worse, when you add in the $800 a month they’re spending on groceries, 84% of their take home pay is gone.

That’s a stressful situation to be in for anyone, let alone someone with a young baby and a long commute time.

And what if something goes wrong or there’s an emergency?

She IS struggling, and it DOES suck.

So naturally she wants things to be different. Who wouldn’t?

If life were rosy, she could move to a nice apartment with great heat, in a convenient location that reduces commute times and costs. Daycare would be low cost and at work, or at least on the way to it, or near their apartment to cut down on the commute time. They would have spare money every month to do whatever they like with. They would have savings and investments.

I want that or better for everyone, including Julie. We need to address the social and economic issues that are contributing to this, and worse.

But here’s what caused me to write this post:

She wants to know how to fix her financial life without budgeting better, making more money, going down to one car, changing anything to do with extras like a gym membership, art, and baby programs, or leaving their jobs and support system by moving.

Since she specifically asked for people to say it like it is, here goes:

I can’t suggest anything other than a miracle with those restrictions. Because the thing is…

If you want something to be different in your life, you have to DO something different in your life.

Even if you don’t like some of those things.

Lashing out in frustration and then demanding advice that requires zero change on your part isn’t going to cut it.

Frustration is the first step, sure.

BUT THE VERY NEXT STEP IS A WILLINGNESS TO MAKE CHANGES.

And the step after that is to actually start making them.

If you aren’t willing to make some changes in your life, there aren’t any tips, tricks, or advice that will help you. None. Zip. Nada.

You can read all the articles in the world and they will make no difference.

So you’re left with a choice.

You can live your life feeling angry, helpless, and frustrated, while getting deeper and deeper in debt.

Or you can decide to make some different choices.

Choices that might suck for a while. But they’d be YOUR choices, based on what matters most to you.

If Julie had written me…

If Julie had written me, I would first have said I couldn’t suggest anything unless she was open to making changes.

Then if she’d agreed to at least consider changing a few things, I would have asked for more information to get a better idea of her situation.

I would have asked questions like these, for example:

- Where does she live? What does she like & dislike about it?

- How old is the 2nd car, since the first one is 10?

- How much could she sell both cars for today if she had to? Could she sell the car that’s worth the most, buy a less expensive one, and use the difference to pay down debt?

- Why is their car insurance so high? What could they do to reduce it?

- What are they buying at the grocery store, and how could they spend less there?

- How about lunches at work — what do they eat?

- Do they do meal planning with an eye to spending less?

- Has she gotten on waiting lists for less expensive or at least closer daycares? Considered sharing a nanny with other families?

- What kind of life does she want to have for her child?

- Do any of her coworkers or her husband’s coworkers live along the same route?

- How far away is her husband’s job? Is biking a possibility? Could her husband work from home part of the time too?

- Does she usually get a tax refund?

- What would her life be like without debt?

- What would her life be like with an extra $1000 a month, or with $1000 less in expenses?

- Etc.

I’d have had a whole slew of questions.

I imagine she might have felt uncomfortable even hearing the questions, let alone considering even DOING anything because of them.

Sometimes people find questions judgmental, but there are no values attached to questions. They’re just food for thought or requests for information, and it can help to have an outsider asking them.

(My entire LIFE changed once because of a question someone asked me about groceries! I’m not going to go into details, but I’m not even kidding.)

The point is, being willing to explore all possibilities is important, and that starts with asking questions and doing some what-if-ing.

Talking and thinking about things doesn’t mean you have to do them. It means you’re considering options.

After those questions…

Sadly at the end of those questions, my tips for Julie would still have been generic in a sense, and related to my life and experiences.

That’s because I can only say what I would do in her financial situation, and I am not her. I can’t give specific advice, so I would have also made the same suggestion Andy did: to see someone knowledgable that is familiar with her exact situation.

But maybe Julie would have started seeing possibilities that she felt might be an option for her.

Because it’s her life. My goal would only to have been to get her thinking about options vs. feeling helpless and angry.

She could then decide what’s best for her, and what actions she’s willing to take. Or not.

So what kinds of things could help?

If you make good money but aren’t even up to the paycheck-to-paycheck point yet, here are some very generic, non-bootstrappy tips that could help.

- Track your spending. (Both daily going forward and retrospectively to see what’s happened in the past.)

- Decide what’s most important to you. And I don’t just mean what’s most important to you that you’re spending money on. I mean overall too.

- Keep the things you love, but pay less for them, find ways to get them for free, or find ways to get paid to do them.

- Say no to the things you don’t.

- Find ways to earn more.

- Find ways to reduce your top 2-4 biggest expenses (or a whole bunch of smaller ones) to give yourself some wiggle room in the budget.

- Use the extra room to get out of debt, which will free up still more room later.

I’m sure just reading that list isn’t super helpful at first glance.

But if you break the items down into specifics that apply to the things in your life, they could be.

IF you don’t have “well but I can’t do that because”-itis.

And that’s the key.

You can do a whole lot of things, if you have to, or if you want something else badly enough.

For instance, I am terrified of falling, but I have no doubt that I would do everything in my power to cross a board between two high rise buildings if it meant saving my son’s life. I would do it, because nothing is more important.

Nothing.

There is no “oh I could never do that because I’m afraid of falling and might die…”

There are no excuses. No complaints.

I would just do it.

Of course, I truly hope a situation like that never happens because just writing this scares me a lot. And by scares me a lot I mean the idea of my son’s life ever being in danger is terrifying. The fear in the pit of my stomach is real. I don’t even want to leave these words in here.

Sometimes, though, taking things to an extreme can give you some perspective.

Think of whatever scares you most, and then imagine what would cause you to do it anyway.

How does that fearful scenario sound compared to…cutting some costs and making more money?

Maybe some changes could be on the table after all.

And change doesn’t require you to feel any particular way about it.

You can love it, hate it, or be somewhere in the middle.

Change just requires you to do it.

If you want something different, you have to do something different.

Let’s go back to Julie and her expenses real quick.

Take her phone bill, for example. Julie’s family is spending $250 a month on phones, and she has a note that they require them:

“2 personal my work phone I require since I’m home 2 days”

It’s not clear to me whether they have 2 phones or 3, but either way it sounds as if she’s mentally written off spending $250 a month on phones as a required expense and moved on.

But, you know what? No one is forcing her to do that. That’s extremely high.

I pay $43.56 for a lot of data for my iPhone, plus unlimited texting and calls. Even putting two phones on that plan would save her $162.88 a month. (And you can get cell service even cheaper than what I’m paying.)

But if you write off even the possibility of doing anything about it, you never will. You’ll continue spending $3,000 a year on phones instead of SAVING $1954.56 a year or more.

So it pays to put everything on the table and see what you could do about it.

Apply the same process to every other expense you want to keep.

Find savings by shopping around, asking for discounts, or maybe sharing or getting things for free. You could even eliminate some things, at least on a trial basis.

Because you know what? If you hate not having those things and would rather feel frustrated, discouraged,and short of money every month, you can always go back to them.

Or maybe you could brainstorm even more options.

Don’t cut everything fun, by any means, because we all need fun and relaxation in our lives. But pay less or nothing for everything you can!

Here are some more ideas that could help.

Taking a look at each specific area of how you earn money and how you spend it can help close the gap. Here are a few more places where Julie might be able to make changes:

Making more money:

- Try and get raises at your current jobs. Then try again on a regular basis.

- Or try to get higher paying jobs elsewhere, ideally that are closer to where you live or allow you to work from home all of the time.

- Or get a different job, and use that to get a matching or better raise in your current job, if you love it. A company I worked for once told me they couldn’t give a raise, but they found the money after I found a better offer. I ended up with a 5 figure raise and more vacation time.

- Try getting a second job, or a side hustle that doesn’t require you to spend money or put wear and tear on a car. Like walking dogs or freelance writing.

- Make sure you’re taking advantage of every tax break that could put more money in your pocket, like using a Dependent Care Flexible Spending Account if you’re eligible.

- If you normally get a large refund every year at tax time, maybe reduce your tax withholding just a little so you still get a refund but also have a tiny bit more take-home pay.

Reducing housing expenses:

Consider possible changes to where you live, like:

- Getting a roommate at your current place. (For example, someone you know. Maybe someone that wants to make extra money babysitting, even. I had a roommate when my son was young, and it worked out well.)

- Changing to a much less expensive 1 bedroom. Sure, it’s nice for babies to have their own room or to have an office when working from home, but those things aren’t necessary.

- Getting free or reduced rent in exchange for management duties if you live in a small complex or rent from someone with multiple properties.

- Moving in with friends or relatives for a while, saving each other money.

- Moving to a different apartment in your same area (since things change all the time)

- Or yes, possibly even moving to a new city that you would enjoy. (Is there really only one place in the entire world you might enjoy living? Maybe your support system would love to live elsewhere too, but they’re sticking around because they want to be close to you.)

- Staying where you are, fixing the cracks in the walls and putting film on the windows to reduce heating costs, and cutting elsewhere instead.

Reducing other expenses:

- Cut the grocery bill significantly. $800 a month is a LOT for 2 adults and a baby, especially since that’s just for groceries. There’s a LOT of room for savings there. Meal plan with an eye toward reducing spending and stretching meals. Eliminate most meat & milk, take advantage of any produce rescues near you, etc. You might even be able to get some food for free, as people occasionally give food away in local Buy Nothing groups. Even if you have special nutrition requirements, you can probably spend a whole lot less. (See this post for some inspiration.)

- Shop around for car insurance. While you’re at it, shop around for better rates for the same services on every single thing you spend money on regularly.

- See if your state offers universal pre-k for when your child gets a little older. Send them to public school when they’re old enough.

- Try to carpool even part of the way to work.

- See this post for many more money saving tips.

There are lots of options, including doing nothing. You just have to find the ones that work for you.

But it can take some time to discover that.

Moving past frustration

I do have a lot of empathy for Julie and others like her.

I’m definitely not going to tell her to “Do better”, even though she requested that from Andy.

Because that sounds a little like “well, you wouldn’t be in this situation if only you’d do better.” The thing is, I don’t think anyone deliberately tries to be in a bad situation. Who would want that?

Many many people, including Julie, work hard and still struggle.

They are doing the best they know how with what they have to work with, and trying to improve.

And I don’t want to say “well some people have it worse” (even though they do; there’s pretty much always someone who has it worse) as if that makes Julie’s situation better.

Because it doesn’t.

I want to say that the world needs to change, for the better, and we are the ones who can make it happen.

We have to move past frustration and into action. Get help when we need it, and help each other when we can. We have to change things, and advocate for better.

It starts with us.

Great response Jackie. It is a very tough situation that Julie is in AND a lot of our country.

Perhaps it’s blind ambition, but I like to think there’s always a way to improve. It might not happen today, but small incremental improvements can help us get where we want to go.

Yes, incremental improvements make SUCH a difference!

we have 2 decent cars. gas and insurance is about 240 combined and i think the insurance part is high. i like you said doing nothing is an option. y’know how many people have been at our house and they didn’t know i write about personal finance? 75% of them say “i could use some help on that.” and i always tell them i’m willing to help get them started with some easy steps like the ones you mentioned like figuring out the cost of their lives, looking at income/lifestyle, etc. they never follow up.

It takes a lot of motivation to change, but I feel like if people DO finally get started, it gets easier and easier as time goes on. But it’s up to them.

Great post w/ rational ideas. A majority of problems do start with expectations – the “I can’t because” you mentioned. And they’re usually linked with “shoulds” – as in things should be one way or another. Those two mindsets reinforce once another, and distort our viewpoints. Like you said, change starts with us. And the first thing we must do is get real with ourselves…which is the change that requires the most effort!

Oh yes! That does require a lot of effort. Sometimes it helps to get an outside perspective too :)

Great response! Unfortunately, life is NOT easy or fair as much as we desperately wish it to be. Its really tough out there and its important to sympathy and empathy to anyone who is feeling frustrated. It really is SO HARD and the choices and decisions we make are not easy or fun.

I completely agree, and I hope things improve for everyone going through tough times.

There is a mental problem of feeling a failure which the feeds hopelessness lethargy apathy.

Yes, feelings like that can be hard to deal with. It’s important to remember though that things can improve too, given enough time.